Publications: Kim, D., Seok, S., & Moon, H. B. (2023). Asset Allocation Strategy based on News Article Sentiment Analysis using BERT and Black-Litterman Model. Korean Journal of Financial Management, 40(5), 155-180.

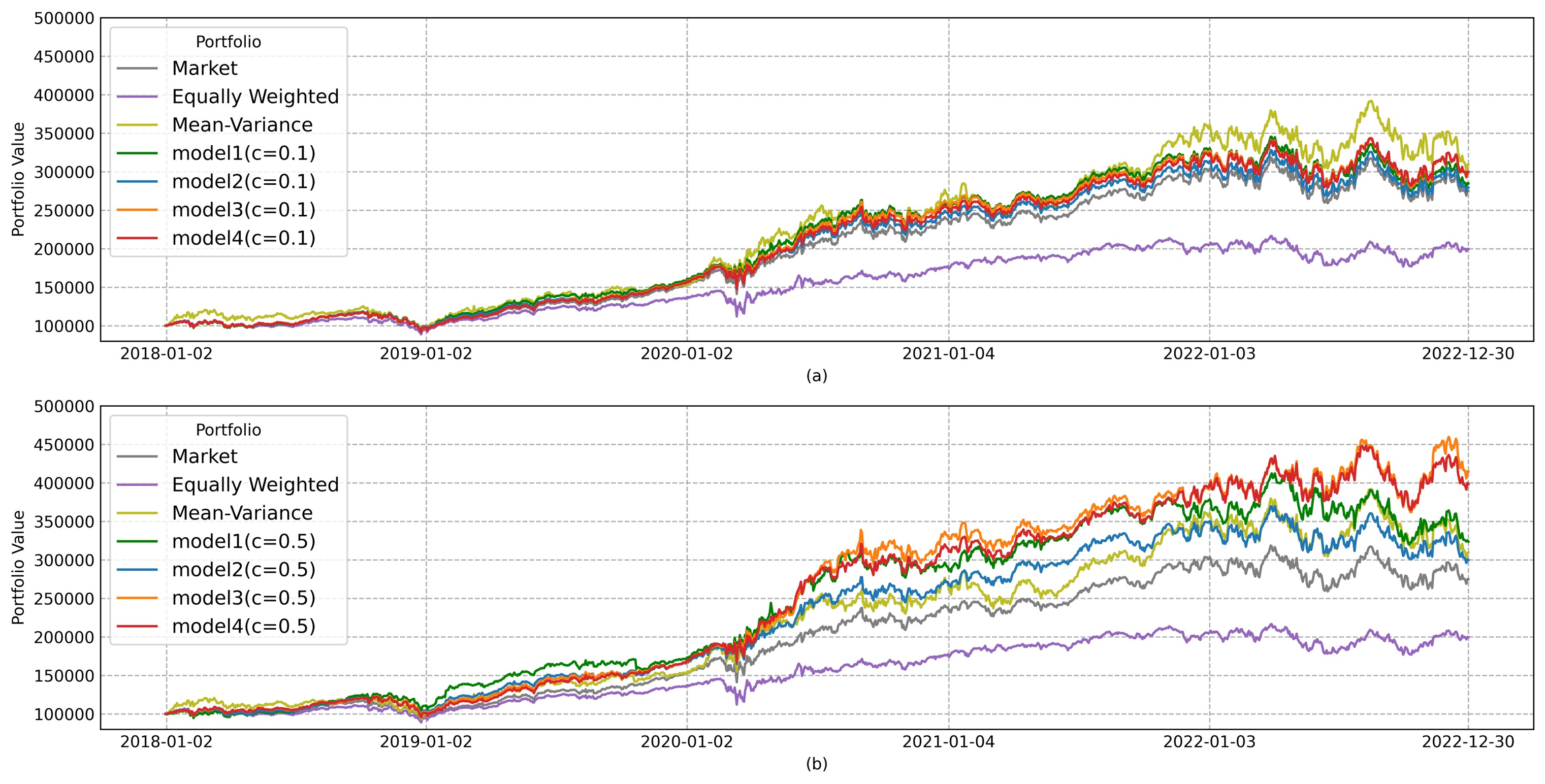

Figure 1. Performance of the Proposed Portfolio (Target Asset: DJI 30)

2310-bert-allocation.md How does public perception and cognitive reaction shape financial markets? This research explores the intersection of human sentiment and quantitative finance, decoding unstructured data to optimize decision-making.📌 The Problem: The Gap Between Sentiment and Quantitative Models

Financial markets are highly sensitive to news and public sentiment. However, traditional portfolio optimization models (like Markowitz’s Mean-Variance model) rely purely on historical quantitative data (prices and volatility). They struggle to systematically incorporate forward-looking, unstructured qualitative information—such as the daily cognitive reaction of the market to breaking news.

⚙️ The Method: Bridging NLP with the Black-Litterman Model

To bridge this gap, I developed an integrated pipeline that quantifies human sentiment and injects it into a rigorous financial model. [Image of Black-Litterman model integration with sentiment analysis pipeline]

- Sentiment Quantification via BERT: Leveraged the BERT (Bidirectional Encoder Representations from Transformers) model to perform deep semantic analysis on publicly available financial news articles. This converted unstructured text into a quantifiable “Sentiment Score” to effectively circumvent the limitations tied to subjective investor judgment.

- The Black-Litterman Integration: The Black-Litterman model is unique because it allows investors to combine market equilibrium with subjective “views.” I structurally transformed the BERT-derived objective sentiment scores into these mathematical views, effectively translating human cognitive reactions into actionable portfolio weights.

🚀 The Impact: Cognitive-Driven Portfolio Optimization

- Enhanced Returns: Demonstrated that a portfolio dynamically adjusted by NLP-driven sentiment outperforms the market portfolio, equally-weighted portfolio, and traditional mean-variance portfolio.

- Sentiment Polarity Optimization: The study discovered that constructing portfolios based on the polarity of sentiment (positive/negative), rather than its intensity, and excluding neutral news articles significantly improves overall profitability.

- Foundation for Behavioral Intelligence: This research serves as an early blueprint for my core methodology: taking unstructured human reactions and engineering them into precise, data-driven decision engines.